Senior Product Designer - Fintech

Designing systems

that move money

and protect people.

12+ years in fintech, I work where complex regulation meets millions of users who need to trust what they see.

About

I turn regulatory constraints

into user-centered products.

Over a decade designing inside the constraints that make fintech hard: regulation, fraud, scale, and risk. Most of my work involves decisions that do not have a right answer.

Worked with teams at Nubank, Ualá and BBVA, leading design for products used by millions across LATAM.

Selected work

Three projects.

Three levels of complexity.

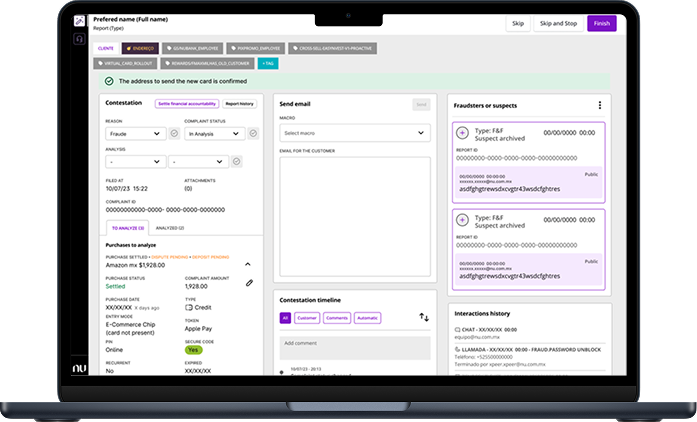

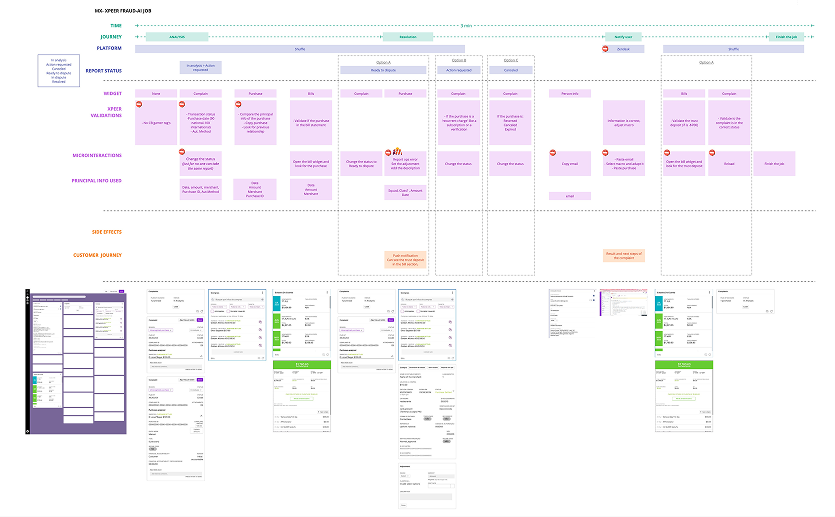

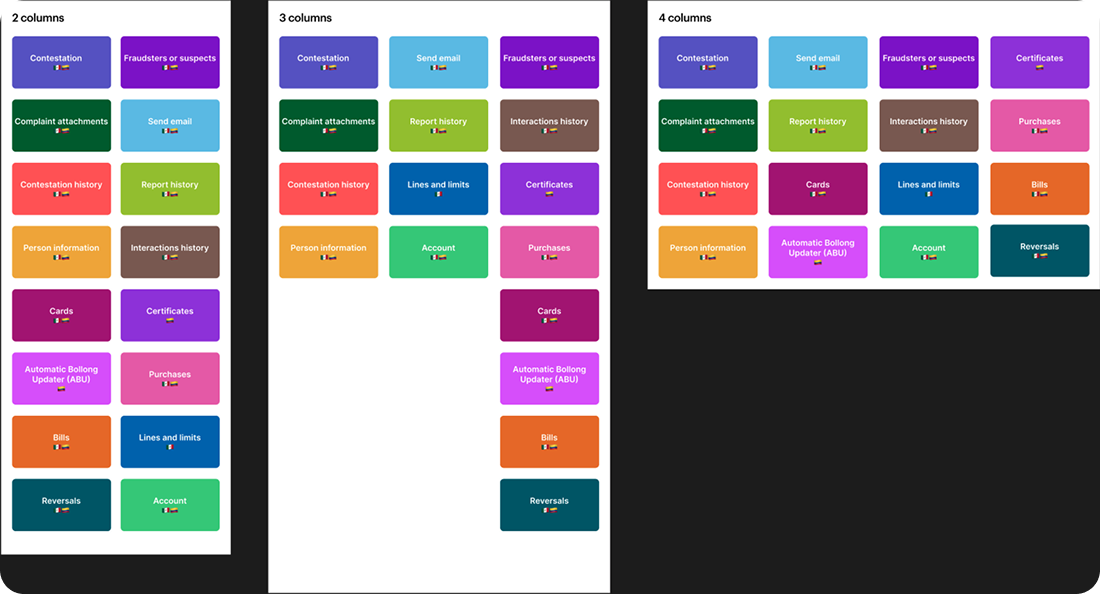

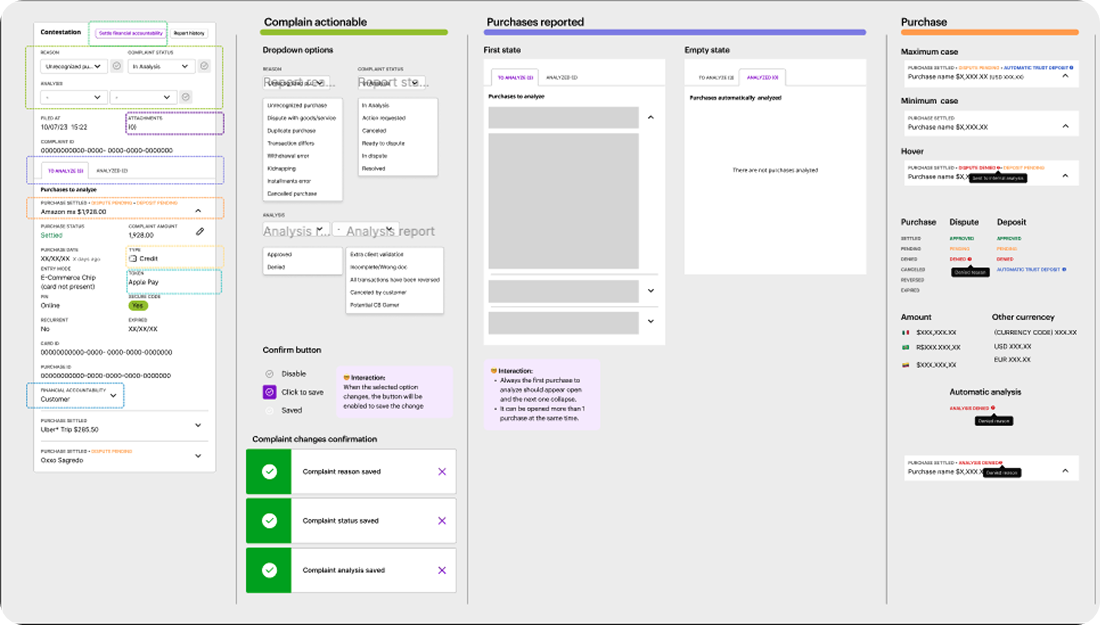

Internal tooling - Fraud Ops - High complexity

Chargebacks Platform

A modular ops platform that reduced fraud agent response times and standardized a fragmented global workflow.

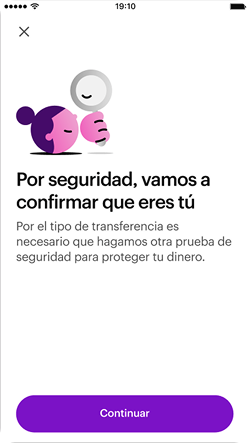

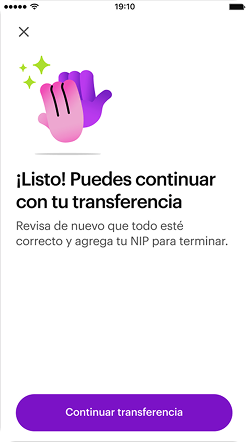

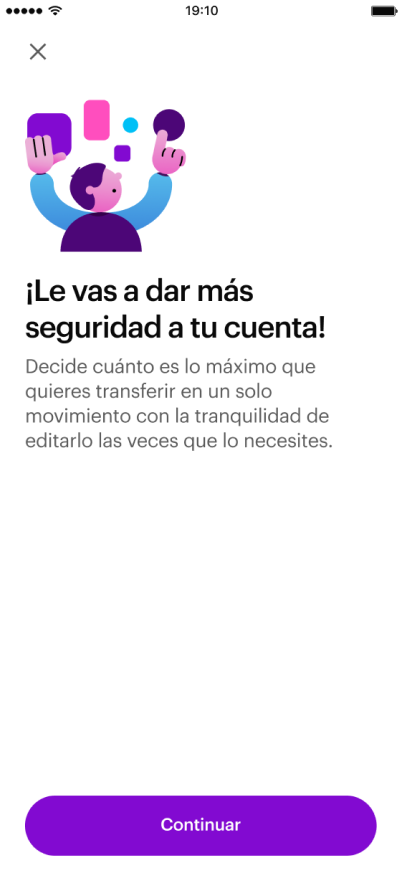

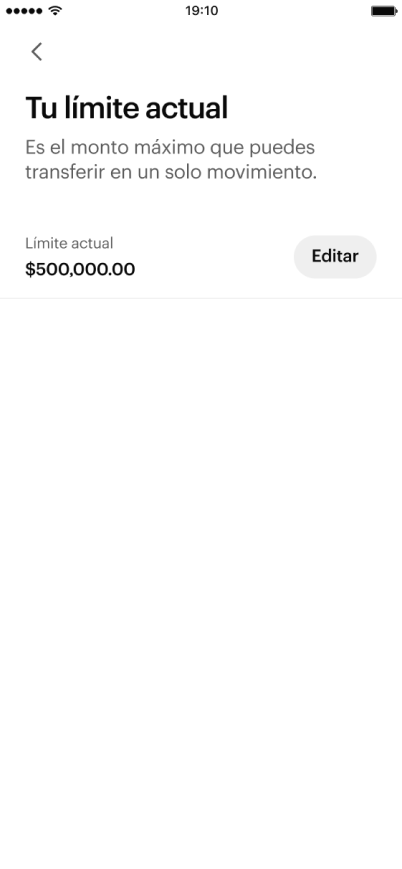

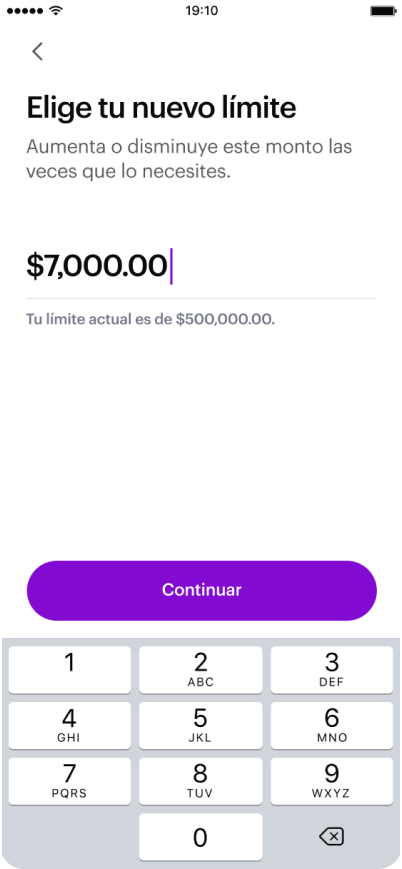

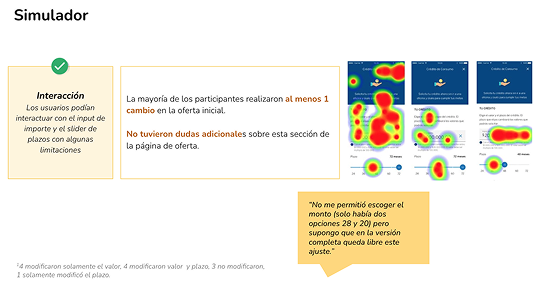

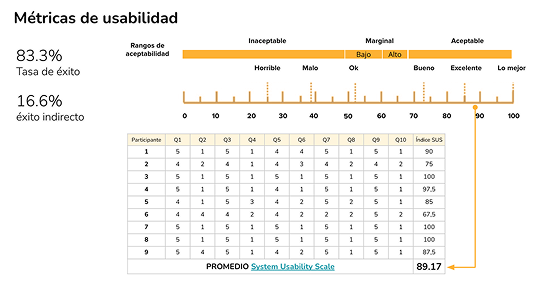

Consumer product - Security - Regulatory

Transfer Limits

A user-facing security flow balancing regulatory compliance with usability. Covers 7M+ users.

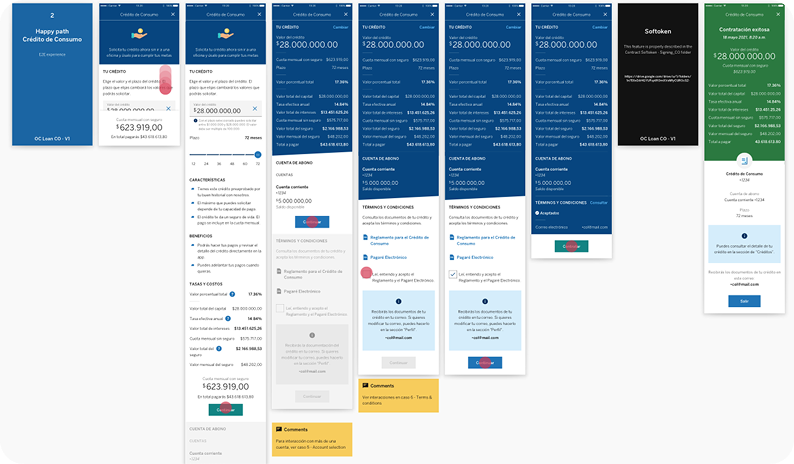

Design systems - Loans - High complexity

Global Loans

A scalable modular loan contracting flow for BBVA adaptable across 5+ LATAM countries. Reduced time-to-market.